This blog sets out the budget policy changes that took place during and after the chaos of the Truss administration; it explores the current levels of social security in the UK and a comparison of these levels with other countries; it examines the extent of welfare cuts since 2010; considers some options which we are led to believe that Sunak and Hunt are looking at and concludes with some alternative options which would lead to a fairer distribution of wealth.

A decade on from austerity 1.0, we are clearly being prepped for austerity 2.0 with the same old line about ‘difficult decisions’ having to be made. Why is it always the case that the difficult decisions made by Conservative governments always adversely impact the most vulnerable in our society, rather than those with the broadest shoulders?

I would suggest that the day-to-day decisions that are already being made by millions of people across the UK, even before winter has set in, are by several degrees far more ‘difficult’ than policy decisions made by Government Ministers detached from the daily grind of life. In the current whirlwind that passes for the current Tory administrations, it is difficult to keep track of the latest giveaways to the rich. However, after the dust has settled on the Truss/Kwarteng ‘free market’ experiment on the UK public, we are left with the following:

| Pre Kwartweng | Truss/Kwarteng mini-budget | Hunt reset |

| Corporation Tax 25% from April 2023 | 19% from April 2023 | 25% from April 2023 (19% for small profits) |

| Income Tax (currently 20%) 19% from April 2024 | 19% from April 2023 | 20% from April 2023 |

| National Insurance 13.25% | 12% from November 2022 | 12% |

| Bank Corporation Tax Surcharge 3% from April 2023 (gross rate 28%) | 8% from April 2023 (gross rate 27%) | Not known |

| Benefit rises – in line with CPI inflation | no commitment | no commitment |

| Pensions ‘triple lock’ – in line with CPI inflation from April 2023 | no commitment | in line with CPI inflation (Liz Truss PMQs 19th October 2022) |

So, as it stands at the moment, we are broadly in the same position as we were prior to the debacle of the Truss Premiership. However, the current government administration led by Sunak is clearly signposting significant cuts to public services and is carefully avoiding any commitment to raising social security or pensions in line with inflation.

It is a moot point now, but it is worth stating that Kwarteng’s mini-budget giveaways to the rich were not balanced by a similar generosity to the least well-off in our society. Kwarteng was also very careful not to give any assurances that benefits were to rise in line with inflation, seemingly content to give up any pretence of us all being in this together.

Current benefit and pension rates

Before we look at Sunak’s options, let’s look at some examples of the current levels of social security and pensions provided in the UK, how it compares with other countries and how policy decisions made by the Coalition and Conservative governments since 2010 have impacted benefits.

Standard Universal Credit Allowance £334.91 single (per month)

Standard Universal Credit Allowance £525.72 as a couple (per month)

Statutory Sick Pay £99.35 per week (for 28 weeks)

‘New Style’ Jobseekers Allowance £77.00 per week (£61.05 if aged under 25)

New (full) State Pension £185.15 per week

A full list of benefit rates for 2022/2023 compiled by the AgeUK charity can be found here and a benefits calculator found here.

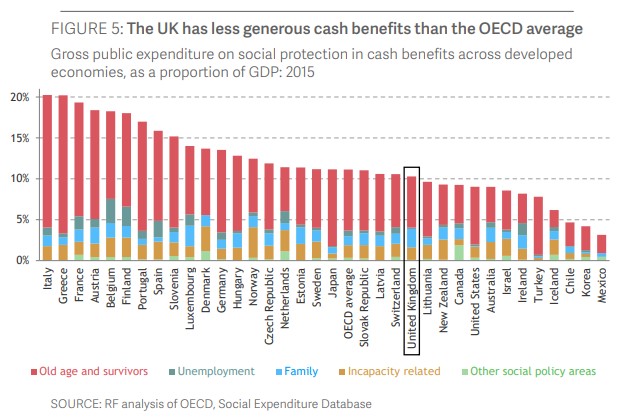

Comparing UK welfare rates to other countries

Comparing the UK welfare state to other countries is challenging due to the complex nature of differing social security systems in each country and their balance of private and public spending across different policy areas. However, in cash-benefit terms (excluding benefits in kind, such as private pensions and public healthcare provision) the UK is less generous than the Organisation for Economic Co-operation and Development (OECD) average.

Sick Pay

Statutory Sick Pay in the UK is set at a flat rate of £99.35 per week (not including any additional sick pay provision within an employment contract) which is payable for 28 weeks. In Germany, sick pay is paid at between 70-100% of full pay for up to 84 weeks. Norway pays 100% for 52 weeks and the Netherlands 70% of full pay for 104 weeks. The rates and length of sick pay for each country in Europe (data from May 2021) can be found here.

Unemployment benefit

New Jobseekers Allowance is set at a flat rate of £77.00 per week for those aged 25 or over. This works out to approximately 13% of the average annual salary in the UK. In France, unemployed people receive 57% of their normal salary, in Germany, they receive 66% and in Italy 75%.

Pensions

In regard to pensions, the UK is once again some way down the table of OECD countries. The UK has a ‘net pension replacement rate’ (the percentage of pension received in comparison to previous earnings) of 58%. This compares to the EU average of 68%. The full set of data from the House of Commons Library research briefing ‘Pensions: International Comparisons’ can be found here.

UK welfare cuts since 2010

According to the Resolution Foundation1 the 2010-15 coalition government cut social security spending by £19 billion by 2023-24. This was partly as a result of the switch from the Retail Price Index (RPI) to the Consumer Price Index (CPI) for the annual uprating of benefits as well as subsequent below inflation uprating. This was offset by £1.6 billion due to increased spending on free school meals for infants and the extension of free childcare to two year olds in lower-income families.

The 2015 budget announced further reductions in working age benefits worth £14 billion by 2023-24. These cuts included the ‘two child’ limit for benefit claims, a four-year benefit freeze, a reduction in the benefit cap (see below) and a reduction in income thresholds in tax credits and work allowances in Universal Credit. From this budget followed the ‘Welfare Reform and Work Act 2016’. For balance I should point out that most Labour MPs abstained when it was voted on in the House of Commons and arguably the fallout from this had a significant impact on the direction of the Labour Party in subsequent years.

Since then, there have been some additional spending by the Conservative government, including a reduction in the Universal Credit (UC) taper rate (the amount of UC withdrawn per each pound of income earned) and an increase in UC work allowances (the amount that can be earned before the taper comes into effect). However, the impact of the previous measures, termed ‘flow measures’ as they only affect new claims, so take many years before their full impact is felt, has resulted in a significant real terms reduction in benefit levels.

The Benefit Cap

The benefit cap, the maximum a household can receive in benefits, was introduced in 2013. Originally the cap was set at £26,000 a year for a family. In 2016, via the ‘Welfare Reform and Work Act’ the cap was lowered to £23,000 for families in London and £20,000 for families outside of London. The benefit cap has remained frozen at these levels ever since.

Each year the cap remains fixed in cash terms, it loses value in real terms. Higher levels of inflation accelerate this trend. Based on current inflation forecasts the value of the cap will have declined by 26%. As of May 2022, around 130,000 households were subject to the Benefit Cap. Of these 87% were families with children and 69% were single parent families. When benefits are uprated, these households will see no increase in the amount they receive despite the rising cost of living.

If benefit rates are increased by 10% in April 2023, in line with the September 2022 CPI figure, and the benefit cap remains at the same level, House of Commons Library research indicates that another 45,000 extra households will have their benefits capped.

What is the plan?

With current estimates of the black hole in the public’s finances ranging between £35 billion to £72 billion, Sunak and his Chancellor Jeremy Hunt face ‘difficult choices’ required to fill this hole and meet the fiscal rules of balancing the books by 2027/28. How they choose to do this will impact all of us one way or another over the coming years and Sunak’s newly found brand of ‘compassionate conservatism’ will be put to a very early test.

Sunak’s botched ‘Energy Profits Levy’ where the ‘super deduction’ investment allowance, quite apart from promoting fossil fuel extraction, resulted in energy companies using the loophole to avoid paying any windfall tax, further dents the Tory claims that they should be trusted on the economy.

George Osborne’s austerity 1.0 from 2010 onwards was based on an 80:20 ratio of spending cuts vs tax rises. After 12 years of Tory austerity, there is little skin on the bone of public services, real terms benefit cuts will send thousands more into poverty and tax rises clash with ‘low tax, small state’ Tory ideology. Sources close to Hunt suggest that the spending cuts vs tax rises ratio will be in the region of a 50:50 split. All will be revealed on 17th November and a slightly improved financial picture, following the turmoil of the Truss/Kwarteng induced chaos, may give a little breathing space.

Hunt has been careful not to guarantee that benefits would rise in line with inflation from next April or that the ‘triple lock’ on pensions would be retained. Another option supposedly on the table is a four-year freeze on tax allowances and thresholds, which would drag many people into paying income tax for the first time, or place people already paying income tax into a higher tax band. Hunt may also look at cutting ‘day to day’ spending as well as ‘capital’ spending (spending for investment) although he will be aware that cuts to capital spending risk impacting future growth. Finally, another area Hunt may look at is retaining the cut to the Overseas Aid budget, due to be returned to 0.7% of GDP in 2024.

An alternative approach

While we may have moved on from the brief Truss/Kwarteng ideology of ‘trickle-down economics’ which regarded ‘redistribution’ with some horror, unless it was a shift in wealth to the rich, we should be wary of things being that much different under the Sunak/Hunt regime.

It is clear to most people that austerity has never really gone away, and local council and government departments are at the limit of what can be cut without severely detrimental impacts on the fabric of our society. Domestically, as the cold weather approaches and with energy prices double that of last winter, we can reflect back on a lost decade of opportunities to insulate the UK’s housing stock, the abandoning of the ‘zero carbon homes’ plan, the botched grant schemes and the lack of support, both in financial terms as well as through building regulations, for domestic renewable energy generation.

Below are some alternatives, setting out both where tax increases could be applied and how benefits could be up-rated, enabling a fairer distribution of tax and wealth.

Tax

- Wealth Tax – while Rishi Sunak may not be in favour, in July 2020 he said: ‘No, I do not believe that now is the time, or ever would be the time, for a wealth tax.’ the idea is getting more traction as the UK’s financial challenges increase and wealth inequality has risen. The ‘Wealth tax Commission’ was established in the Spring of 2020 and its report was released in December 2020. The report established that for a number of reasons a one-off wealth tax would be preferential to an annual wealth tax. The amount a wealth tax would raise is dependent upon a variety of factors, including to what threshold of wealth the tax would apply. The report sets out that setting a 1% rate for wealth of £1 million could raise £147 billion. The report also addresses concerns about liquidity (asset-rich, cash-poor) as well as fairness and avoidance. You can read an Executive summary (11 pages) of the report here or the full report here. There is also an FAQs that answers the top questions raised about a one-off wealth tax which you can read here.

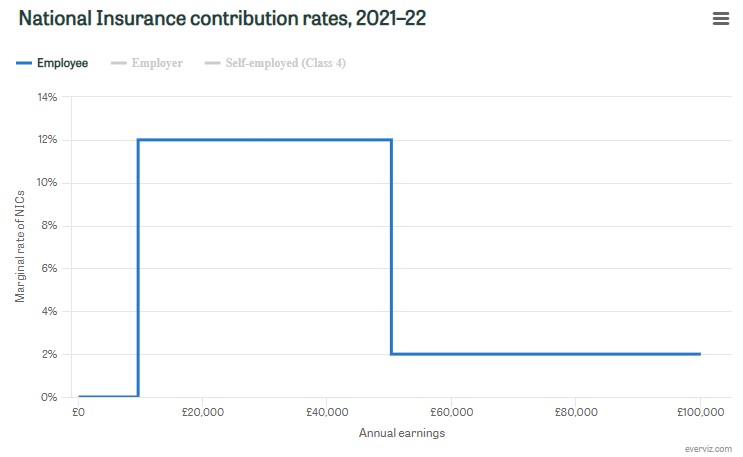

- National Insurance Upper Earnings Limit – currently (until November 2022) the National Insurance rate for earnings between £12,570 (the primary threshold) and £50,270 (the upper earnings limit) is set at 13.25%. For earnings above this upper earnings limit, the rate of National Insurance deducted drops to 3.25%. From November 2022 these rates are due to drop to 12% and 2% respectively, the same rates as shown in the chart below. This drop means that proportionally the richest are contributing a significantly smaller percentage of their income in National Insurance than those on lower incomes.

This reduction in the NI rate at the £50,270 threshold aligns with the higher tax rate threshold at which point income tax increases from 20% to 40%. Apart from this making a strong case for a single tax, this does result in a combined marginal tax rate that varies little between those earning £51,000 a year and those earning £2 million a year. For example, from November 2022:

- those earning £20,000 would pay a marginal rate of 32%.

- those earning £51,000 a year would pay a marginal tax rate of 42%

- those earning £151,000 a year would pay a marginal tax rate of 42%

- an individual earning £2 million would pay a marginal tax rate of 47%

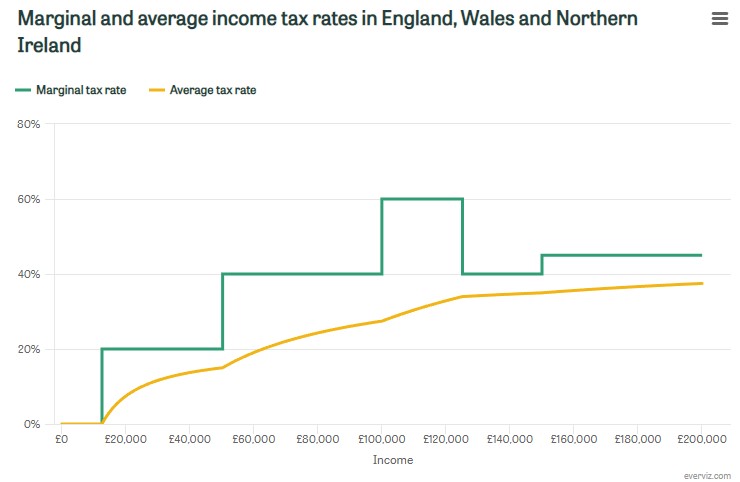

A fairer tax system would increase the marginal tax rate at progressively higher rates of income, rather than the current flat rate above £150,000. This could be achieved in any number of different ways. To avoid the anomalies around the £50,000 and £100,000 areas, due to the ‘High Income Child Benefit Charge’ and loss of Personal Allowance, a higher rate of National Insurance could be introduced at the £150,000 threshold. There are approximately 629,000 people in the UK who earn over £150,0002.

- Capital Gains Tax – CGT is a tax on the profit of an asset you sell that has increased in value. As recently as 2015 this tax was applied at 28% for the higher rate and 18% for the lower rate. In 2016 these rates were reduced by the then Chancellor George Osborne to 20% and 10%. These rates could be raised to bring them more in line with the current income tax rates of 20% for basic rate taxpayers and 40% for higher rate taxpayers. It has been estimated that this change could bring in around £3.5 billion extra a year.

- Bank Surcharge – this is an additional tax levied on the profits of banks on top of the current rate of Corporation Tax. Currently, Corporation Tax is at 19% and the Bank Surcharge is set at 8% – a combined rate of 27%. Sunak had set out in the Spring 2022 budget a plan to increase Corporation Tax to 25% in April 2023 and reduce the Bank Surcharge to 3% – an effective combined rate of 28%. Sunak has the option to maintain the Surcharge at 8% leading to an effective combined rate of 33%. He could also reduce the increase in the Surcharge Allowance, which was due to be increased from £25 million to £100 million.

- Windfall Tax – Prior to ‘Energy Profits Levy’, introduced earlier this year, Sunak couldn’t bring himself to call it a windfall tax, oil and gas sector companies paid a headline rate of 40% on their profits. The levy introduced an additional 25% rate, leading to a combined rate of 65%. However, a ‘super deduction’ investment allowance for further oil and gas extraction has resulted in the energy companies taking advantage of this loophole which has resulted in them avoiding any levy payments. This Levy was expected to raise £5 billion in the first 12 months. This loophole has not only resulted in a loss of vital revenue, but has also encouraged further investment in fossil fuel extraction. Norway’s tax rate on North Sea oil and gas firms is 78%. If the UK matched this rate and closed the loophole, research suggests this could raise an additional £6.6 billion pounds a year.

Benefits and Tackling Inequality

- Real Living Wage – The National Living Wage which by law employers must pay is currently £9.50 an hour for those aged 23 or over. The ‘Real Living Wage’ calculated according to the cost of living, based on a basket of household goods and services is currently set at £10.90 an hour, with a higher rate of £11.95 an hour for those working in London. Further, the Real Living Wage is paid at the same rate regardless of age, while the statutory NLW pays a reduced hourly rate for younger people.

The Real Living Wage could be a stepping stone to a £15 minimum wage advocated by the TUC, details of which can be found here.

- Raising the Benefits Cap The benefit cap limiting a cap on household benefits to £26,000 a year for a family and £18,200 a year for a single person was rolled out by the coalition government in 2013. The cap was further reduced by the Conservative government’s 2016 Welfare Reform and Work Bill to £20,000 for a family and £13,400 for a single person outside of London. The cap has been fixed at this level since 2016. As of May 2022, around 130,000 families were subject to the Benefit Cap. Of these, 87% were children and 69% were single-parent families. When benefits are uprated, these families will see no increase in the amount they receive despite the rising cost of living. If benefit rates are increased by 10% next April the House of Commons Library estimates that up to 45,000 extra households may have their benefits capped. This cap both increases inequality and poverty across the UK. As the table below shows, if CPI inflation uprating had been applied to the benefits frozen by the Conservative government, the Benefits Cap would now be £22,435 for a family and £15,032 for a single person outside of London, with higher rates for those in London.

- Ending the ‘two-child limit‘ The two-child limit was introduced in 2016 by the Conservative government. This legislation means that third or subsequent children born after 6th April 2017 will not entitle the claimant (the parent or parents) to any additional amount of benefits. The Universal Credit child element in 2022/23 is £244.58 a month for each child not affected by the two-child limit. As of April 2021, 317,500 families, with a total of 1,138,650 children were affected by the limit. The Child Poverty Action Group (CPAG) estimates that by the time it is fully rolled out, 3 million children will be affected. Removing the two-child limit would lift 250,000 children out of poverty, and lessen the depth of poverty for another 600,000 children at a cost of £1 billion, according to an analysis by the CPAG. Sara Ogilvie Director of Policy, Rights and Advocacy at CPAG says: “The two-child limit is a brutal policy that punishes children simply for having brothers and sisters. It forces families to survive on less than they need, and with soaring living costs the hardship and hunger these families face will only intensify. Government must abolish this senseless policy, and protect children from a lifetime of struggle.”

Conclusion

In a vain attempt at brevity, I have not covered all the issues that lie ahead for many over the coming months. Social rents (which potentially could have increased by 11% in April 2023) but will now be capped at between 3% and 7% will impact the most economically challenged in our communities. The Energy Price Guarantee will now end in March 2023 and be replaced by more targeted support for the most vulnerable households will be an economic shock for many. I would suggest that he concentrates significant support on the 4.5 million people who pay for their energy via prepayment meter. The ‘Minimum Income Floor’ for self-employed people claiming Universal Credit was reinstated in August 2021 and many are facing significant financial difficulties as a result.

Lord King, former Bank of England governor, and who earned around £300,000 a year in that role, said last week “So we may need to confront the need to have significantly higher taxes on the average person. There isn’t enough money there amongst the rich to get it back.” As Mandy Rice-Davies said, “Well, he would say that, wouldn’t he”.

Sunak certainly has tricky choices to make. As a Tory, he will instinctively recoil from placing the burden on the rich, and he will be aware of how unpopular this would be within his divided Party. However, twelve years of Tory austerity has decimated public services and slashed social security support. If he chooses to place the burden on these areas with further cuts, quite apart from the damage to our services and a detrimental impact on our economy, the political backlash will be significant and potentially fatal.

This time Labour must resist falling in behind any repeat of the narrative the Tories successfully peddled for their first round of austerity, the burden of which fell on the poorest in our society, the effects of which are still being felt today. The coming years present significant challenges, but they also present an opportunity to build a fairer society, built on a just transition to a green economy, with a government that displays empathy and compassion. After 12 years of the current government, it is clear we are not going to get any of this under the Tories.

Apologies if this blog has been a rather gloomy and statistic-heavy read. I am aware that behind every benefit cut is a family struggling to make ends meet and, despite how those on benefits are portrayed in the media, many are working people just trying to get by and do the best for themselves and their families. However, while politicians on all sides talk about supporting ‘hard workers’ we should never forget those who through bad luck, ill health, or other circumstances are unable to work, either in the short-term or long-term. I believe we should judge our society by how we support the most vulnerable people within it.

Finally, on a slightly lighter note. If Sunak does want to provide a little Christmas cheer, he could do with looking at upping the rate of the Christmas Bonus, which has been frozen at £10 since 1977!

Julian Vaughan

1st November 2022

Sources and further reading

Resolution Foundation: The Long Squeeze October 2022

House of Commons Library; The impact of the two-child limit in Universal Credit

Wealth tax Commission: A wealth tax for the UK – Executive Summary

Prof Prem Sikka: We can raise lots of money without taxing the masses

4 thoughts on “Who will bear the burden of Sunak’s ‘difficult decisions’?”